Investment Horizon: 4-5 years

When the Cambridge Analytical crisis first shocked the Internet, it naturally piqued my interest on Facebook and I started to have the idea of conducting research on it. One of my motive of analysing Facebook as a company is to look for investment opportunity and another contributing factor is to sharpen and bulk up my investment acumen (For the past two years I’m spending much of my time and concentration on my studies and also learning fundamental knowledge about psychology, investing, finance and economics through various books). Since I’ve just finished my SAT test in May and have plenty of time while waiting for my first IB semester to commence, I decided to take a serious and holistic analysis on Facebook, spending my time on meaningful activities.

Throughout the process of conducting research on Facebook, I’ve met some obstacles that prevents me from getting data that I needed in order to arrive at a better and more sound conclusion, and also realise some of my weaknesses that hinder me from being better informed and make the best investment decision possible. Nevertheless, I give you my word that this piece of analysis is definitely well-conducted after hours of thinking and judgement. You are welcomed to give constructive feedbacks and speak up your opinions if you held a different view. As I’ve always believed, thoughtful disagreement is the path to understanding the truth better. I will address the shortcomings of the analysis and my weaknesses in the next post so that everyone get a chance to learn from it.

Before I start, I’ll note that this is a lengthy analysis and it may be boring to read for some of you. For those who want to save their time and jump straight to the conclusion, here’s it:

- Facebook Inc is a company with sound financials, competent management and solid fundamentals (although it has weakened compared to the totally dominant position it enjoyed few years ago)

- The current price (as of 6 July 2018) is slightly stretched and I believe that there will be better buying opportunity in the future 1-2 years due to potential economic headwinds

With all these being said, I shall start my analysis now.

Concept Glossary

I may use some terms and concepts that some readers may not understand. Hence, I will try to clarify these ideas here so that it will be easier for you to grasp their meaning and understand my points better.

Gresham’s Law: Originally applied in Economics, it states that bad currency drives good currency out of the system. Here, I use this law to depict the scenario that bad players in an ecosystem drive good players out of it

Critical point: An extremely important juncture in a company/system which is critical to the operations and success of the company/system

Divine Discontent: A concept that I’ve learned from the thought-provoking blog by Ben Thompson, Stratechery, which states that consumers always have a voracious appetite for a better product, they will never be fully satisfied and stop pursuing a better product, thinking that ‘this is enough for me’. For more information about Divine Discontent, you can browse the article at Stratechery

Network Effect: Refers to a positive feedback loop, where positive developments in an area inadvertently leads to positive outcomes in another area and reinforce each other that results in a virtuous loop. It can also works conversely, where negative developments in an area inadvertently leads to negative outcomes in another area and reinforce each other that results in a vicious loop

Critical Mass: the amount of substance needed to force a chain reaction and alter the development of an ecosystem

Positioning 定位: the place that a brand occupies in the mind of the customer and how it is distinguished from products from competitors.

Company Profile

I guess many of you are quite familiar with what Facebook is and what it does so I won’t go into details explaining what Facebook is here. But do you all wonder before that how does Facebook make money? The short answer is, advertisement (which makes up most of its revenue). In fact, Facebook Inc does not only consist if the Facebook app, it also comprises Instagram, WhatsApp, Messenger and Oculus VR. It made many acquisitions in these few years but most of them are of relatively small size and not likely to make a huge impact on the bottom line of the company,rather, more likely to act as complementary product or features to their main products. Therefore, Facebook, Instagram, Messenger, WhatsApp and Oculus VR are collectively known as the Facebook Family of Companies, as per Facebook Inc. The entire monetisation process of Facebook’s business consists of three critical links:

- Maintaining and growing their social media ecosystem

- Obtaining and utilising user data to get meaningful insights

- Placing ads in the social media platform targeted on their user base

I’ll break down these three critical links one by one and explain my analysis on their dynamics and Facebook’s competitive position and performance on each of them.

Maintaining and growing their social media ecosystem

As we’ve all know, Facebook’s social media ecosystem consist of Facebook, Instagram, Messenger and WhatsApp. We shall start with Facebook, as it is the largest among all of them and the primary revenue source for Facebook Inc.

I think everyone on Earth not living under rock should knows what is Facebook and what kind of services does it provide. In a sentence, Facebook is a social media platform which enables people to connect with their friends and families, and keep themselves updated with the lives of their “Facebook Friend”. I think many of you might have already realised that the way you and your friends are using Facebook has undergone a huge shift in the recent few years. In fact, the way people communicated and interacted on Facebook has changed dramatically. Why have all these changes taken place? Before I give out my point of view, let me introduce a few dynamics that are at play in the Facebook ecosystem:

Network Effect (as mentioned in Concept Glossary)

Divine Discontent (as mentioned in Concept Glossary)

Gresham’s Law (as mentioned in Concept Glossary)

Positioning 定位 (as mentioned in Concept Glossary)

Critical Mass (as mentioned in Concept Glossary)

Attention Pie

It won’t be all surprising that there are more and more players coming out of the social network industry such as Twitter, Instagram (owned by Facebook), Snapchat, Musical.ly, Vine etc when you understand three fundamental concepts that shape the dynamics of social media industry: Divine Discontent, Gresham’s Law and the characteristics of the industry. To understand the consumer behaviour of social network users, we must understand that Divine Discontent is at play. Divine Discontent makes us understand that users will never fully satisfied and stay content with a one-size-fit-all app for interacting with their acquaintances. Instead, users will be eager to try out the ‘new thing’ out there for the sake of excitement,curiosity and novelty. What’s more is that, if the new app actually provides an exciting and original experience for users, they will adopt it very quickly. Once the users adopting the new social network app reached a critical mass, the app will soon establish a formidable regional network effect, reinforcing positive outcomes (more users lead to more users).

If Divine Discontent is absent is the social media industry, Facebook would’ve been the only social network platform that exist: People can type 140 characters in Facebook, yet they still use Twitter; people can upload pictures and videos on Facebook, yet they still use Instagram; teens can send selfies to their friends using Facebook Messenger, yet they still love Snapchat.

Another important force that contributes to the fragmentation of social media apps is the characteristics of the social media sector: low switching cost, low loyalty, low stickiness. Creating a new account in a new social media app isn’t a painstaking and troublesome process: Fill in your email address, set your password. As simple as that and you have a new account now! People won’t have any second thoughts before trying out the hottest social media app because is is free, and most importantly, the existing app they are using is free too. No sunk-cost fallacy playing out here. That’s why once a new social media app can grab the attention of consumers in a short period of time and establish a regional network effect, it has the potential to grow into a formidable force that wakes up the social network behemoths at night. The golden goose lies in establishing a wide network effect. Low loyalty and low stickiness is the product of zero sunk-cost, zero opportunity cost and Divine Discontent.

The third law active in social media platforms is Gresham’s Law. Bad players drive good players in the ecosystem out. The bad players here have a slightly nuanced definition. ‘Bad players’ here refers to players whose existence will irritate a substantial group of users and nudge them to spend less and less time on the social media platform (thus triggering a reversed network effect and starting a vicious cycle if the critical mass is reached). Bad players, therefore, includes spam bots, excessive advertisements, fraudsters and also middle-aged parents and elderly. Middle-aged parents and elderly are considered as bad players because they are one of the catalysts that drive down the engagement time of teen users and millennials on Facebook. The large influx of middle-ages and elderly into Facebook prompt young users to feel that Facebook isn’t as ‘cool’ as it is before anymore and their actions,speeches and thoughts are not unrestricted as before. Facebook is no longer the place where they can say anything or post anything unfettered anymore. There are eyes watching on them now.

A large part due to the dynamics of Divine Discontent and Gresham’s Law, specialisation is an inevitable outcome in the sector (I apologise for yet another self-invented terminology here). Specialisation means that each social media app occupies a special place in the users’ mind for their different core functions, meaning that each app specialises in different scenarios and uses. To give you several examples here:

App: Instagram Position: Following friend’s lives and uploading pictures

App: Snapchat Position: Selfie-oriented messaging and uploading moments of real life

App: Twitter Position: Following celebrities, viral trends and relevant topics

With these dynamics in mind, we have the tools needed to make sense out of the development of the Facebook ecosystem these few years. In their early days, Facebook was the active community for young users to express their thoughts and feelings. However, later on, the influx of middle-ages and elderly (bad players in this context) and the Divine Discontent dynamics at play gradually causes young users to spend lesser time on the social network and put more of their time on other social media apps such as Instagram and Snapchat. Middle-aged and elderly groups are a growing share of Facebook’s user’s demographic and the position of Facebook in the mind of teen users and millennials is growing weaker and weaker, as is it not the only social network that they are using anymore. Many more choices are in the market now. They are more willing to spend their time on Instagram and Snapchat relative to Facebook.

Although it’s good news that Facebook is encompassing more users from larger age groups, constantly declining interest of young age groups in Facebook is still a problem that can’t be ignored, as they still constitutes a large part of Facebook’s user base. To add insult to injury, the dynamics of network effect at play is also slowly reversing: when your friends post more thoughts and share more feelings on Facebook, you will naturally spend more time on Facebook engaging with them. If the activities of your intimate friends of Facebook decline, you will also naturally spend less time on Facebook, diverting the attention to the social networks where you friends are active on. To counter this situation, Facebook decided to channel their resources and attention to two elements that will, in their hope, rekindle the interest of younger age groups on Facebook and make Facebook an active community again as it once was.

The two elements are videos and news.

That’s why in the past two or three years, your news feed is flooded with news and interesting videos instead of your friends’ feelings and thoughts. There are two reasons that shape these changes. One of them is that users already rarely share their thoughts and feelings on Facebook anymore, another is Facebook’s effort to make a news-and-videos-oriented news feed, its goal is to attract users to spend more time on the platform consuming news and video content instead of engaging with friends in the old way. This is a huge gamble, and it works. Although injecting many news in their news feed algorithm does cost them a lot of problem and even harm its brand image (fake news scandal flooding everywhere), although younger age groups still spend more time engaging with friends on Snapchat and Instagram, and even though users don’t actively engage with each others and share their thoughts as active as they used to, Facebook manage to curb the declining interest of teens and millennials, and re-occupy its unique place in users’ mind, albeit by news-and-videos-oriented content. Facebook users engage on their platform, but in a more passive way, through video-sharing and news-sharing, and also tagging friends on content they find interesting. Furthermore, Facebook is growing its presence and market share in developing countries and Asia Pacific region, especially Indonesia and India. Later, Facebook also double its effort on Facebook Groups, emphasizing it more than ever. It succeeded in creating active local and regional groups on Facebook, building a strong and active regional-based group and interest-based group on its platform.

Facebook can never go back the the platform it once used to be, but it somehow manage to reposition itself and establish a new life for itself and its users.

In 2012, Facebook spent 1B dollars to acquire Instagram. In retrospect, that is an enormously wise decision from Mark Zuckerberg and Co. It would cost Facebook billions of ad revenues if it continues to let Instagram grow into its own social giant.

Instagram is a photo and video-sharing social network that is immensely poplar among youngsters, and most of its users are in the 18-29 age group. As of September 2017, it has reached 800 million Monthly Active Users (MAU) and a whopping 500 million Daily Active Users (DAU). As you may have expected, the dynamics of Divine Discontent, Gresham’s Law and the characteristics of the social media industry is also present in Instagram.

There are a few points I would like to highlight here about Instagram and its future potential (these are not backed by any statistics and are assumptions made based on its similar development to that of Facebook).

Primo, although Instagram is already fairly penetrated in the U.S, Canada and western countries, we can still expect to see it enjoying decent growth in Asia Pacific region and other countries in the world, especially developing countries such as Indonesia and India. With that being said, I believe that it will follow a path similar to Facebook’s monetisation process, in which a substantial amount of ad revenue generated will be from advertisers in U.S, Canada and the West. Even though the share of ad revenue generated from Rest of World (all countries excluding U.S, Canada and Europe) is going to increase slowly over time, it is believed that over the next five years, the majority of ad revenue based on advertiser geography will be from those three regions aforementioned. This causes a noticeable disparity as the major user growth comes from APAC region and developing nations, while the major advertising revenue comes from advertisers in the U.S, Canada and Europe. The same scenario can be observed in the case of Facebook too. More on that later.

Secondo, Instagram is enjoying a near duopoly in early-age users’ preference for social media platform with Snapchat (although Snapchat still have a relatively narrow user base and geographic presence). Its ad revenue as of 2017 is $3.64B, a relatively meagre figure as compared to Facebook Inc’s total revenue of approximately $40B. In spite of that, Instagram’s astonishing growth rate and under-utilisation will allow it to grow its revenue to at least over $10B (a very conservative figure) in the next 5 years. It will be the fastest revenue growth engine in the entire Facebook money-making machine over the next 5 years.

WhatsApp and Messenger

Facebook bought WhatsApp in February 2014 for $19 billion. On the other hand, in-app messaging had always been one of the functions of Facebook in the early days, until it spin this function out and create a separate app solely for messaging purposes called Messenger.

If we compare them side by side, WhatsApp and Messenger each have 1.2B users worldwide. WhatsApp has gained its users over the years, loved by users for its slick interface and user-friendliness. Meanwhile, Messenger managed to gain its clout in a short period of time primarily by leveraging the massive user base of Facebook, which has about 2B Monthly Active Users. 2.4 billion users certainly signifies a large treasure trove for monetisation opportunities for Facebook Inc in its future, however, it’s not a low-hanging fruit for Facebook, and definitely a challenge to Facebook’s management to convert their large user base into lucrative sources of profits. It’s not an impossible task, but the doors left open for monetisation is very limited.

Why is it that hard to make money off messaging apps as compared to social network apps? We must first contemplate consumers’ behaviour while they are using apps for intimate communication with acquaintances. I’ll try to illustrate multiple scenarios to give you an idea of what I’m trying to bring up.

Imagine this scenario, where you are going out with your family and you are sitting in the car looking outside of the car windows. You saw billboards and giant LED screens displaying ads throughout the journey. Do they irritate you? Absolutely no.

Now you are in the cinema, you can’t wait any longer to watch the latest superhero films. But you need to wait for 20 minutes of ads display before the movie starts. Do you feel irritated? Most likely no, and most of the time the ads are interesting!

You are swiping through your News Feed and Instagram feed, almost after swiping through six or seven posts some ads might be shown to you. It may irritates you sometimes but if it’s relevant, you’ll be okay with it most of the time.

And now, you are chatting with your best friend on WhatsApp, or having some serious talk with your boss to work out a solution, you will be offended by display ads in your chat list, or even worse, pop-up ads. Other types of ads such as banner ads are also not appealing to users at all.

The point of listing so many examples here is that the more private and more intimate a thing is to users, the more sensitive they are to objects that intrude their space, which is deemed to be private by them. Therefore, it’s very hard for Facebook to insert ads into Messenger and WhatsApp and can account for only limited potential ad revenue.

Generally speaking, the most important thing that communications app can have is their access to users’ data and messages. Nevertheless, the plausibility of Facebook using users’ messages and data to target ads on users is getting lesser and lesser. Facebook once tried to do that, leaving users no option but to consent to handing over their private messages to Facebook for business purposes if they wanted to continue using WhatsApp’s services. That is proven to be a grave mistake as it causes a massive backlash and lambastes among users around the world. WhatsApp later have no other way but to renounce its decision to sooth the public anger and retain users. Furthermore, the GDPR regulations that was rolled out on May also clearly stated that WhatsApp can only operate in the region if only it respects user data and its services be provided unconditional of users’ consent to the way data will be handled.

If primarily making money off Messenger and WhatsApp with ads is not an option, what other business models can be applied to these two messaging apps for monetisation purpose? Introducing app-related merchandise can be a viable model (as proven by the success of Line in Japan and Taiwan and KakaoTalk in South Korea), but Facebook doesn’t seem to be taking this commercialisation path into consideration. A tantalising and possible alternative is adopting Wechat’s model, which leverages its dominance in communications to build many more services around its app, such as its Wechat Business Platform, Wechat Pay, and Wechat Blogs to form an indisputable ecosystem. However, Facebook also doesn’t seem to be keen on adopting this kind of business model, not announcing or signalling such plans in their financial reports. To be fair, there’s also some feasible reasons behind their decisions. WhatsApp was built on the notion of providing a private,messaging-only interface for users. In addition, its competitive advantage lies in its smooth usability and slick interface. Fitting it into the an-app-for-all model as that of Wechat will probably diminish its usability advantage and causes frustration among its users, who are accustomed to its nimbleness and appreciate it. Besides, the huge cultural differences between Western users and Chinese users means that the success of such a business model in China doesn’t guarantee its success in other parts of the world.

With all these said, is Facebook’s $19B acquisition of WhatsApp a complete mistake? Absolutely not, WhatsApp is more of a strategic purchase that allows Facebook to access the communications market out of America and in other parts of the world. WhatsApp and Messenger will still yield a lot of business opportunities in the future, but as of now and the next few years, monetisation opportunities are limited and therefore, WhatsApp and Messenger won’t be discussed in the remaining part of this analysis anymore.

Obtaining and utilising user data to get meaningful insights

The core value of Facebook lies in its data – and its massive user data comes from its web traffic. As we have already analysed the fundamental characteristics and traffic of Facebook, Instagram, WhatsApp and Messenger above, this part will be a discussion of Facebook’s ability to collect and aggregate user data. Because the main profit engine of Facebook Inc is its Facebook app and Instagram app, we will be emphasizing on these two apps (WhatsApp and Messenger doesn’t collect their users’ messages for targeting purposes).

If you’ve always wondered why Facebook and Instagram can show you relevant ads most of the time, take a look at the amount of data it collects though your activities on their apps: your posts, your videos, your IP address, your handheld device, your interest, your likes, your shared posts, your contact list, your payment history, your search history etc. It probably know you better than yourself. What’s more is that it can even know which website you have just browsed if the websites choose to install Facebook Pixel! It is almost undeniable that Facebook has the most complete set of user data among all websites and apps that profits primarily from adverts, except Google.

But an aspect that couldn’t be ignored is the ability that Facebook possess to collect user data as freely as they want to. Last time, Internet companies including Facebook can take advantage of the ignorance of their users and obscure ad preferences settings. Consent to give away all your account data to Facebook is the default option of every user account. Privacy policies are hard to understand using abstract languages, and that doesn’t matter to most users, as they simply click ‘Agree’ to the privacy policy of every app most of the time.

Things started to change about two years ago. More and more privacy activists are ranting and criticising the shady practices of Internet Giants to keep their users in sleep. Increasing number of uses start to pay attention to what Facebook is doing with their data. The issue of user privacy came to a crescendo in 2018 after the Cambridge Analytica scandal emerged on the headlines of all presses. Shortly after that, the General Data Privacy Regulation (GDPR) was officially rolled out in Europe (Yes, the rule that causes ur mailbox to be flooded with privacy policy updates emails). The strictness of GDPR rules has conveyed European regulators’ attitude towards tech giants that breach users’ data. The fine of noncompliance to GDPR can go up to 20 million Euros or 4 percent of annual global turnover, whichever of both is highest. Apart from that, the current regulation states clearly that pre-ticked boxes or any other method of default consent is no longer allowed and explicit and clear consent is required from users. Also, consent to processing a precondition of a service must be avoided, meaning that irregardless of whether consent is given, services must still be provided to all users equally. All of these rules signifies a large shift: the power of obtaining data by Internet companies is going to gradually diminish, and the the power of controlling their own data by users is increasing.

It means that tech giants can no longer avoid clear communications with their users and they must obtain user consent in an explicit manner. Does that mean game over for Facebook and its peers? Far from it. There are two forces working in the favour of Facebook: user ignorance and user laziness. Even though awareness about user privacy has increased in the recent years, the majority if internet users still remain oblivious to the rights that they have towards their data and the obligations that tech companies need to fulfil. They still possess the thinking that if they do not agree to the those privacy policies, they won’t get to enjoy the free services of Google, Facebook and Instagram anymore. Hence the only way is to give all their data out. Although after some time most users may be aware of their rights and power, it’s likely that they still won’t deny Facebook’s access to their data, simply because they don’t feel the need to do it. They won’t be willing to spend even a fraction of their time to re-adjust their ad preferences. They also don’t feel that it’s a big deal to give away their data to tech companies, it’s not like the tech companies will sell their data to fraudsters and criminals. Even if tech companies hand user data to government for national security purposes, they will think that:”at least I’m not the only one!”.

Based on these two factors, I infer that over the next few years, user consent to obtain data won’t be a problem that threatens Facebook ads model. In some sense, GDPR may even be a plus for Facebook (more on that later). However, user sentiment definitely poses potential risk to undermine Facebook’s ad business. As mentioned above, users won’t deny Facebook’s access to their data, simply because they don’t feel the need to do it. Once they are triggered and feel that giving away their data could put them in a disadvantaged position, the outcomes will be altered very quickly, and Facebook is doomed to fail in the case of a massive data-bank run.

In short, obtaining user data is believed to be smooth and not a problem in the future, but a time bomb such as this must be monitored and contemplated meticulously from time to time.

Placing ads in the social media platform targeted on their user base

Now comes the integral part of Facebook’s money-making machine. The ability to convert user data into insights for advertisers and convert services provided into ad products is the primary source of Facebook’s ad revenue (Apart from advertising revenue, Facebook also makes money from in-app payments and Facebook games. But it wont be part of the analysis because the contribution of payments revenue is immaterial to Facebook Inc’s total revenue).

To understand the entire digital advertising landscape, let us from explore it from the perspective of an advertiser. Next, we will have an overall view of Facebook’s ad network briefly and move on to the factors that shape the advertising industry.

Advertiser Incentives

As known by everyone, an advertiser’s main objective will always be obtaining the highest return-on-spending on their ads. In a world with perfectly rational agents, advertisers will keep searching for as many publishers that offer the potential of great return-on-ad-spending, test their ads on all of those publisher’s ad inventories, and finally choose to advertise with publishers that offer the highest return-on-ad -spending. However, in reality, advertisers will simply choose several reliable and reputable ads publisher to advertise their products/services. Later, the advertisers will likely stick to the publishers that offers the best results out of the several publishers that they’ve worked with and allocate more budgets to the publisher with great results.

Facebook Ad Network

Diagram: Facebook’s Ad Network

As seen above, Facebook advertising network comprises of two main parts: Facebook Business Pages, which enables businesses to connect directly with consumers, and Facebook Ads, which enables businesses to advertise on their ecosystem. The ecosystem includes Instagram, Facebook, Messenger and Facebook Audience Network (FAN). In addition, FAN includes the Facebook Instant Articles network, a feature in the Facebook app, third-party apps and websites which collaborated with Facebook and depended on Facebook to channel ads into their websites and apps, and also in-video streaming ads, which insert ads in videos played on Facebook. I won’t dive deep into what the Facebook Instant Articles network is, but here’s a brief excerpt from Wikipedia that sums it up pretty clearly:

Instant Articles is a feature from social networking company Facebook for use with collaborating news and content publishers, that the publisher can choose to use for articles they select. When a publisher selects an article for Instant Articles, people browsing Facebook in its mobile app can see the entire article within Facebook’s app, with formatting very similar to that on the publisher’s website

To get a more in-depth view of what the Instant Articles is, you can browse its page on Facebook if you want to.

Facebook usually recommends advertisers to advertise on the entire Facebook Ad Network, allowing Facebook’s algorithm to place advertisers’ ads in the Facebook Ad Network accordingly, instead of the advertisers themselves choosing where to place the ads on their own. By doing so, Facebook is able to bundle the inferior and cheaper FAN ads with better quality, more expensive native ads on Facebook and Instagram as a package. As Facebook native ads and Instagram native ads are the core products and core competencies of Facebook Inc’s product offerings, we will only be emphasizing on the two products mentioned above in our research piece.

After having a simplistic view on advertisers’ decision making process and the Facebook Ad Network, we will introduce the factors that shape the advertising industry, and discuss various important aspects and topics revolving the aforementioned factors that characterises the industry.

Advertising Industry Dynamics

There are three primary factors that constitutes that supply and demand of ads inventory of different ad publishers: traffic, data and ad elements

Traffic is the king of advertising. Think of why advertising has shifted away from traditional media such as billboards, television, radio broadcasting, newspapers to Internet platforms such as Google, Facebook and Youtube. In traditional media, the number of people and potential customers that can be reached is relatively limited. For instance, there’s a ceiling in the number of people that will pass by the billboard everyday due to geographical constraints. There’s also a ceiling in the number of people that read a particular newspaper in a single day, given that most of its customers are locals. The advent of the Internet opens up a whole new world, enabling Internet users around the world to connect to various websites irregardless of their nationality and geographies. This, alone, magnifies the opportunities and traffic of Internet platforms as compared to traditional advertising options. In effect, advertisers can increase their return on ad-spending multiple folds higher at a cheaper price and with a more scalable method if they opt to advertise with Internet companies. All this is only made possible with the robust web traffic of Internet platforms.

It’s because traffic is the core value in the entire advertising value chain, a ‘smiling curve‘ can be observed here:

Diagram: Ad Publishers command the greatest power in the smiling curve

The second dynamic that affects the supply and demand of different ad inventories is user data. The reason why Google can charge higher on their ads as compared to Facebook is because of the user data they command. Imagine how much Google know about its users when it knows what you want to ask even before you finish typing what you want in the search bar. This is because when you want to know about everything, you ask Google before anyone else. You want to have lunch in a nearby Japanese restaurant, you Googled. You are searching for a white collar t shirt, you Googled. You want to know more about programming languages and take up an online programming course, you Googled. With an unprecedented amount of user data and the accuracy and reliability of it, it gains a strong foothold in the advertising industry, owning about 43% of market share.

The third factor that governs the advertising sector is the required elements to have effective ads and directly links to the return of spending on ads. The underpinnings of successful ads comprises of at least one of these five elements:

- Super-exposure

- Perfect crowd targeting

- Retargeting

- The State of Nonchalance

- Super-Interactiveness

Super-exposure

Super-exposure is derived from a concept in psychology named the ‘mere exposure effect’. ‘Super-exposure’ points out that the targeted customers must be exposed to the relevant ads at least seven times to catch the attention of targeted customers and occupy a position in their mind to generate awareness towards a brand. Examples of success are ubiquitous billboards with the same ads and TV ads where the ads are often circulated in a long enough time period and many enough times to induce brand awareness

Perfect lookalike targeting

Crowd targeting, which is also named as ‘lookalike targeting’ means modelling customer groups with shared characteristics and behaviour, and place ads that are targeted towards this customer group. Judging by its name, you can know that perfect lookalike targeting simply means a publisher that enables a near-perfect targeting ability of the customer groups. For example, niche magazines such as TopGear(an automobile magazine) has a very specific customer group: Males that are obsessed towards the automobile industry, familiar with it and love getting the latest updates in the industry. The ad inventories of this magazine is naturally tantalising to automobile spare part suppliers and automobile manufacturers because of its niche crowd that enables perfect crowd targeting.

Retargeting

Retargeting is a form of online targeted advertising by which online advertising is targeted to consumers based on their previous Internet actions. Many ad-based websites now offer retargeting service. Facebook Pixel is a great example of retargeting. Once you saw an ad, clicked on the ad and is redirected to the advertiser’s website, Facebook Pixel will know that you’ve shown interest in the ads. Later, Facebook will show you tailored ads of the previous website specifically targeted to potential customers that engaged with the ads before, as they are more likely to be converted into sales than those users who never engaged with the ads at all. In this piece of analysis, Google’s superior ‘demand fulfilling ads’ that drives instant conversion of sales are also classified under the retargeting element.

The State of Nonchalance (TSON)

‘The State of Nonchalance’ is one of my observations of user behaviour and another term coined by myself. TSON is the state where users do not have an end goal in mind or carrying out any task at the moment the ads are displayed towards them. Instead, users are on a casual state of mind and feeling relaxed while the ads are displayed to them. A great example of TSON is Facebook native ads, which is ads displayed on Facebook news feed. While Facebook users are swiping through their news feed, they are usually in a casual and relaxed mood, which helps in the absorption of ads. A product which possess the opposite element on TSON is ads displayed on Instant Articles. Users who are browsing Instant Articles are committed to an end goal: finish the article they want to read. Therefore, the readers will swipe over the display ads on the article page before the ads can finish loading on the page.

Super-Interactiveness

Super-interactive ads are ads that are creative, lively, and attractive enough to grab the audiences’ eyeballs, aka ‘the ads that are so interesting you don’t even want to skip it’. Ads that are very creative and nice to watch are often extremely rare, but the format of the ads will also greatly increase the attractiveness of your ads. For example, video ads and interactive Snapchat filter ads are definitely more enjoying to be shown as compared to typical display ads and banner ads. That’s also why video is becoming increasingly popular with ad publishers

Phew… Finally, we’ve finished going through all the elements for successful ads. Let’s move to the next part and examine the competition map of Facebook Inc’s ad products.

Competition Map (对位图)

Facebook Inc’s competition can mainly come from two areas: revenue allotted to traditional ad publishers and ad revenue distributed to it among ad publishers that provide awareness ads.

Any one who is attentive and observant in their lives can definitely identify the tailwind working in Facebook’s favour: the decline in usage of traditional media (which are also traditional ad publishers). More and more people are cutting the cords; Newspaper circulation are declining at a steady rate. Let’s not forget,again, that Traffic is the king of advertising. It can be logically reasoned that more and more share of the ad revenue pie will inevitably go to digital advertising.

Diagram: Competition Map (对位图)

P.S: Sorry for the messy side notes and scribbles on the draft, just kindly ignore it

Because the main goal of all advertisers is to convert ads spending into sales, the more likely an ad can drive conversion, the higher the price of the ad inventory. Therefore, ads can generally be differentiated into two types: ads that drive brand awareness (awareness ads), which is cheap and ads that drive instant conversion (conversion ads). The marketing funnel can help us to understand this better. As the funnel goes down, the more valuable the elements is.

After all the previous discussions, we have already known that Facebook ads are awareness ads. Its native ads, Instagram’s native ads and ads on FAN works primarily to deepen brand awareness on consumers’ mind. Now, let us examine which of the ads elements does Facebook native ads possessed.

- Super-exposure

- Facebook and Instagram’s news feed enable native ads to be displayed to targeted users for several times when users are swiping through their news feed continuously

- Perfect crowd targeting

- While Facebook’s crowd targeting is not perfect, it currently offers one of the best and the most accurate lookalike targeting option due to the massive user data that it has from its large user base. Although it can be argues that other niche ad publishers such as trade magazines offer even better and a more specific crowd that Facebook, their ads monetisation opportunity is also fairly limited due to its niche customer group. In stark contrast, Facebook encompasses crowds and customer segments of different age groups, characteristics, behaviour and interests. The combination of a broad user base and refined user data enables one of the best targeting service coupled with the broadest customer groups among all publishers

- Retargeting

- While Google is the indisputable champion in driving instant conversions, Facebook is also improving on driving conversions through better retargeting efforts. Its new ads format such as the Dynamic Ads series and tools for retargeting purposes such as Facebook Pixel have dramatically improved its retargeting ability and move Facebook ads down from the ‘Awareness’ funnel to the ‘Consideration’ funnel.

- The State of Nonchalance

- Facebook and Instagram is one good example of TSON ads. However, most of Facebook Audience Network (FAN) websites,apps and Instant Articles are anything but the antithesis of TSON ads. That’s why FAN ads is cheap and of low-quality. It can only survive through bundling with high quality native ads

- Super-Interactiveness

- While Facebook ads aren’t by any means super-interactive and that type of ads that will make consumers willingly watch it, it is moving towards the correct direction through its evolution of ads type. New ads products introduced following new features introduced (such as Instagram Stories) contributed to more interactive ads. Besides, Facebook evolution from a people-oriented social network to an increasingly video-oriented social network indirectly implies that new video-related ads products will be more interactive and visually appealing. Higher interactivity naturally leads to higher profit margins

In short, all the successful ads elements that Facebook ads possess is the key to its success and having all five elements is its strongest competitive advantage compared to other ad publishers which also compete on the grounds of awareness-driven ads. Facebook is already not merely an awareness-only awards. Facebook and Instagram’s ad products are evolving from the purely awareness funnel more to the consideration funnel through its extremely solid ads elements. That is a great leap towards the path of higher margins. While I won’t go deep into each of Facebook competitors’ profile and analyse them one by one, I do think that there is two competitors worth mentioning individually: Amazon and Programmatic Ads.

Amazon

Although Amazon’s advertising revenue is only 2.5% of its total revenue, it is definitely the 800-pound gorilla that can’t be ignored by the advertising landscape. Its large amount of web traffic and user data comparable to Facebook and Google makes many people thinking that it may be the third-largest dominant force in the digital advertising space. My conclusion here is that Amazon can become a large player in the space of advertising, but its direct competition with Facebook is minimal. As previously discussed, Facebook is the kingpin of awareness ads, and Amazon is gaining ground in a different arena. Amazon’s native ads is most compelling to vendors and merchants on Amazon wishing to sell as many of their products to vast Amazon shoppers. Therefore, Amazon’s ad revenue comes from sources in its own ecosystem, consisting primarily vendors of products only on Amazon. Its display ads poses direct competition to Facebook’s FAN. However, we must know that FAN is only a negligible part of Facebook’s revenue sources and Amazon’s display ads is an even smaller portion of its total ad revenue. Some investors also talked about how will Amazon Echo displace Facebook and Google in the advertising industry if its smart speakers become the dominant search engine in the future. I think that is probably not a problem to be worried about in the next 3 to 5 years as even if Amazon’s smart speakers become the dominant search engine, that will most likely take place at least 5 years from now (which is out of the stated investment horizon).

Programmatic Ads

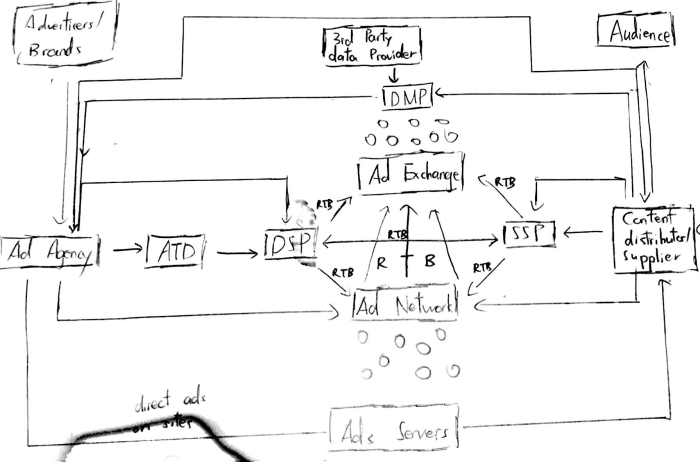

What are programmatic ads? “Programmatic” ad buying typically refers to the use of software and platforms such as Demand-Side Platforms (DSP), Supply-Side Platform (SSPs), and Ad Networks to purchase digital advertising, as opposed to the traditional process that involves RFPs, human negotiations and manual insertion orders. I know this definition doesn’t serve well enough as an explanation at all, and believe it or not, the actual process of programmatic ads buying is even more complicated and convoluted than this. As the saying goes, a picture paints a thousand words.

Diagram: Programmatic ads buying process – involved parties

Although the drawing quality of the diagram is extraordinarily deplorable, I believe 99% of you still won’t really understand the entire programmatic ads buying process after looking at this flow chart (In fact, some media buying agencies also can’t fully understand how the ad buying mechanism works). That doesn’t matter, though. The only thing you need to keep in mind is that the entire programmatic ad buying chain is non-transparent, convoluted and the performance of ads is hard to measure.

The rise of programmatic ads can be attributed to the tremendous shift of ad revenue to digital advertising in recent years. However, there are a few issues that stymies the future growth of programmatic ads and I seriously doubt that they can grow continually at the same growth rate in the previous years.

One of the issues that is plaguing programmatic ads is its opaque buying process through a real-time bidding process. It makes it hard for advertisers to track where their ads are placed and whether their ads are targeted accurately to the desired lookalikes. This make reviewing and measuring ad performance even more difficult. On top of that, the buying process of programmatic ads contains many risk such as frauds, manipulations of performance metrics, and Internet bots performing suspicious activities.

Next, programmatic-ads-buying is a long value chain that typically involves many parties and middleman such as DSPs, SSPs and Ad Exchanges. These middlemen take small slices of the advertising fee respectively. In aggregate, these small slices add up to a big chuck of expenses. The chart below shows how much of the allocated advertising budget set by advertisers get to the hands of ad publishers in the programmatic ads buying process:

To repeat the quote again, Traffic is the king of advertising. That’s why if Facebook and Google build an entirely private advertising ecosystem tailored specifically for their own aka ‘walled gardens’, they are indirectly squeezing the profits of players in the programmatic-buying field. And the two behemoths did exactly this, with Facebook having its own advertising network and Google owning an entire programmatic buying ecosystem of its own. With the ad buying process conducted completely in their own efficiently-run ad ecosystem, the issues of opacity and frauds go down dramatically. Facebook and Google also provide analytics service for advertisers to measure ad performance substantially better. Furthermore, with the vast user data and web traffic they dictate, their native ads are of better quality than 80% of programmatic ads on other websites, as a substantial number of programmatic ads includes low quality ads that doesn’t contain either of the required ad elements.

Diagram: Facebook and Google’s walled garden

Last but not least, the GDPR which comes into effect in May hits not the Internet giants the hardest, but services and platforms revolving the programmatic buying process. As Facebook and Google have direct communication with their users, they are more likely than any other platforms to get users’ consent for advertising purposes. That’s not the case for programmatic buying platforms. They don’t have direct relationship with Internet users and are much more vulnerable to the risk of not being able to gain user data for targeting purposes, which is a major threat to their business model. Although programmatic buying related companies have once and again said that the effect of GDPR in the Eurozone is minimal to them, they are definitely put in a more tight position than either Facebook or Google.

Last Notes

- Facebook Inc still offers the best value for money among the awareness ads landscape for its broad user base and precise targeting

- A continual shift or more ad revenue to digital advertising and the plausible decline of programmatic ads provides room for even more ad revenue growth in the future

- Facebook’s competitive advantage and solid ad elements enables it command more and more high profit margin ad products

- Potential threats from new ads format stemming from disruptive technologies such as AI, Blockchain and VR/AR must be monitored and gauged from time to time. The huge openings and leakages that sink the ship is best detected when they are still small cracks. And for investors, the best thing to do when you see that there are cracks in the ship and the captain (management) is not able to rectify it, is to jump ship before it sinks.

Management

I believe that most of you must be familiar with at least two of the five executives of Facebook Inc: Mark Zuckerberg and Sheryl Sandberg. Anyway, here is a list of the main executives of Facebook Inc:

- Chief Executive Officer, Founder – Mark Zuckerberg

- Chief Operating Officer – Sheryl Sandberg

- Chief Financial Officer – Dave Wehner

- Chief Technology Officer – Mike Schroepfer

- Chief Product Officer – Chris Cox

Facebook Inc’s management has lead Facebook well throughout the years and they definitely have a stellar track record, which is reflected in the stock price. The management team also ensured that the company is efficiently run and financially sound. With these in mind, let us review Facebook’s management’s track record and how they handle things in the past to have a peep on how they will likely perform in the future.

When Instagram first emerged as a nascent social network app, Mark Zuckerberg and Co realised that Instagram has a huge potential to become the next big thing in social media. Its slick and elegant interface, easy-to-use features and photo-sharing characteristics make Instagram the darling of teenagers and millennials. Hence, they decided to bought Instagram in 2013 for $1B. At that time, it may seem like a skeptical acquisition, but in retrospect, this acquisition become one of the most lucrative growth pipeline for Facebook, bought only at a price of $1B.

Facebook’s acquisition of WhatsApp, although costed approximately $22B and is not acquired in its early-stage, does seems like a sensible move too. First come the visionary reason of acquiring WhatsApp, if Mark Zuckerberg’s means it when he said Facebook’s mission is to truly ‘connect the world’, then WhatsApp is a perfect puzzle piece to be fit into the ‘Connect the world’ puzzle of Facebook. It has nearly 600 million of monthly active users as of when it is acquired (source: Statista), what’s more is that WhatsApp’s user base is spread throughout the whole world, complementing Facebook Messenger’s concentrated user base in the U.S. From a perspective of business and strategy, buying WhatsApp prove to be a meaningful move too. Facebook can amass even more user data and information from the vast 600 million WHatsApp users (that is before serious talks of regulations and the insurgence of GDPR). On top of that, WhatsApp can pose potential threats to Facebook as a communication network. For instance, it is in the same advantageous position (possible even more) as Facebook to roll out additional services and features (refer to Wechat’s business model), and extend into many more parts of their users’ life. In spite of the hefty price tag, the WhatsApp move is feasible.

When Snapchat crack into the social media market in its early days, Facebook immediately saw its potential and offered to buy it at a price of $3B in 2013. Nonetheless, Snapchat turned down the offer. Facebook’s solution? Duplicate Snapchat’s most interesting feature in their own social network and modify it to be even better than its predecessor. This strategy, although doesn’t looks good, proved to be a tremendous success. Instagram’s story count now exceeds Snapchat’s story, and time spent on Snapchat has been declining after Instagram rolled out its new ‘Story’ feature. This wounded Snapchat’s core competitiveness and lucrative business opportunities, while helped Facebook Inc to unlock more products for advertisers.

All these successful moves ensured that Facebook enjoyed a near-monopoly dominance in the social media market. A confluence of prudent acquisitions and successful expansion of product features established Facebook’s firm position in the market. This also proves that we can most probably count on Mark Zuckerberg and Co to maintain its dominant position in the social networking industry over the next 5 years.

Facebook is also far-sighted on its future, announcing its 5-year and 10-year development roadmap. Its long-term goal will be betting on Virtual Reality (VR) technology to help connect the world in an even more interactive way. To achieve this, it is spending huge amounts on VR technology and productions of VR content. Although it’s too early to say, Facebook is currently a strong player in the VR-gaming industry and extending its tentacles into day-today applications of VR technology. It also proves that Facebook has a clear direction where it is heading to in the future.

Apart from maintaining its dominance in the social media market, Facebook management also responded well towards scandals and public outrage. The management planted the seed for the fake news scandal and Russian meddling event when it decided to make news one of the pillar of news feed and failing to take the responsibilities of a news publisher in ensuring the credibility of those news. It saw itself as merely a platform for people to disseminate information and not a publisher that makes sure the news on its platform is authentic. The painful consequences such as the outlandish fake news scandal and reports of Russian meddling in the 2016 U.S presidential election makes Facebook realise its grave mistake. To extinguish voices for more regulation on Facebook, Facebook endorsed its role to filter unbelievable information and spend huge sums in its fact-checking programmes to curb the spread of more fake news, fake accounts and political meddling in its platform. Mark Zuckerberg also said that Facebook will focus on fixing these problems in the next three years to sustain the health of its ecosystem. To give him credit, spam accounts and fake news have been steadily declining after Facebook rolled out efforts to put a full-stop on this issue.

Mark Zuckerberg and Co also handled the Cambridge Analytica scandal well enough, managing to sooth the public’s emotion and prevent their worries about privacy from looming big. His testimony in Capitol Hill also fared well, having no regulations imposed to Facebook following his testimony in Congress, while giving the Senators and the public an acceptable explanation of the scandals and attitude towards the data-leakage crisis. Facebook, although had much responsibility in the crisis, was perceived to be more of a victim of the scandal and the company that breached its rules.

Facebook’s management has long known about the importance of gaining user consent for ads targeting. The enforcement of GDPR pushes them even further to consider clear communication and mutual understanding with their users. Therefore, aside from complying with privacy regulations in the Eurozone, Facebook goes a step further to make its data-oriented advertising business model even more transparent to users throughout the world. It reviewed its privacy policy and drafted them using more simple and concise language which users can understand. It also communicated with its users and give them clear information on how they can adjust their ad preferences, what Facebook actually does with their data, and how users can download their data sheet to see what information Facebook has about them. All these new measures regarding data transparency and effective communication with users gives Facebook more cushion to make their users comfortable about handing data to Facebook. This is definitely a smart move and sensible decision-making from management.

Management candour is definitely an essential aspect to all investors. Fortunately, Facebook’s management is honest and open about their goals and financial results with investors. They don’t try to hide anything fishy, mask bad results and dodge questions from investors in earnings calls. They had also always make credible statements about future earnings outlooks and future expenditure projections. As a side note, Facebook has a great track record of management stability, with its executives staying in the company more than 5 years each and low executives turnover.

Facebook has also kept the company well-operated and has built a great company culture to fuel its future development. It continue to be a place that attracts talented employees and guaranteed innovation.

We had reviewed management’s compensation plan and concluded that management compensation is reasonable and that management has aligned incentives with the company’s shareholder. Facebook Inc also has a board filled with prominent directors. Although many of them are from Silicon Valleys and less diversified, we believe that the board of directors carried out their task independently and responsibly, and also did a great job on overseeing management’s performance and decisions. One thing to highlight here is that the CEO and founder of Facebook, Mark Zuckerberg holds more than half of Facebook’s voting right, constituting about 60% of voting power (including proxies). While this means that all of Facebook’s governance and structure is under his absolute power, we believe that as a founder and and major shareholder of the company, Mr Zuckerberg will be a reliable and open-minded leader that will determine the final outcomes that is best for the company. Indeed, no one is more suitable than the founder to have the visualise the company’s future and steer it into a great path.

It is undeniable that Facebook has focused less and put less resources on futuristic ‘moonshot projects’ and extend its arms into other traditional industries such as Google and Amazon. From management’s discussion and their past performances, it can be inferred that they will continue to focus mainly on improving their social network ecosystem and the only huge project on future technology is Oculus VR (even though, strictly speaking, its VR tech is also on connecting the world better), its AR and AI technology are both oriented towards new features on its social network platforms. This makes Facebook to have a relatively lower PE than other tech giants such as Google and Amazon. Although some may view this as not innovative and a minus point, we are comfortable with its conservativeness and give more weigh and attention to Facebook’s ability to constantly improve its ecosystem and comes up with innovative ad products to maintain its dominant position in social media market. (as a reminder, our investment horizon is 4-5 years).

Although the management had committed mistakes over the years, they learned painfully from those past mistakes and took action accordingly to prevent similar issues from happening in the future. Each mistake made them more experienced and careful in their way of handling the Facebook social network ecosystem and their success definitely outweighs their failure. All in all, we are satisfied with Facebook’s management’s performance and we believe that they can be relied to lead Facebook in the future.

Financials

If Facebook’s fundamental soundness is impressive enough, its financial stability will shock you even more. All ratios and measures point to a company will steadily surging profits, zero debt, and healthy cash flows. Its financial soundness is what makes its financial reports so easy to read. Furthermore, clear and concise languages are used throughout its reports, management remarks and comments are candid too. Here is a brief overview of its financial health as of 31 December 2017:

******

Revenue Y-o-Y growth: 47%

EPS Y-o-Y growth: 54%

Free Cash Flow Y-o-Y growth: 50%

Current ratio: 12.9 : 1

Debt / Equity ratio: 0.14

Assets / Liability ratio: 8.3 : 1

Cash Conversion Cycle: 1.14 days

Intangibles / Book Value: 5%

Long-term debt as a % of invested capital: 8%

Cash, Cash Equivalents and Marketable Securities: $41.71 Billion

Operating Cash Flow / Sales: 60%

Operating Cash Flow / Assets used to generate cash flow: 71%

( Assets used to generate cash flow = P&E + Intangibles + Goodwill )

Liability Coverage Ratio: 6.4

% of cash generated by daily operations = 66%

( Operating Cash Flow / Cash inflows from operation, investing and financing activities )

ROA = 18.8%

ROE = 21%

ROIC = 19.7%

* 83% of Facebook’s long-term debt is made up of income tax payables

* No signs of Assets – Liabilities mismatch is found

* Stuck to the same auditor for years and no changes or dubious signals in the auditor’s comments

* Consistent in their accounting principles and measurements of key user metrics

* Most of their marketable securities are divested in liquid financial instruments such as AAA corporate debt, U.S treasuries and government agency treasuries

* No signs of large scale insider-selling / insider-buying activities is observed

******

As shown above, Facebook’s business model enables it to amass large amount of cash that is more than enough to finance its daily operations. Its advantageous cash position also enables it to acquire interested companies without external financing.

As for the costs and expenses of the company, the revenue of Facebook is growing more than its operating expenses every year. Its EBIT as a share of total revenue is growing steadily every year, with a stunning figure of 49.8% for 2017. Such stunning operational efficiency can be achieved a large part owing to its Aggregator characteristics, as defined by Ben Thompson of Stratechery. Facebook spent years building its enormous social media ecosystem and the previous few years are the harvesting year for it. Its industry characteristics and network effect affected its cost structure tremendously: huge upfront infrastructure costs, low customer acquisition cost, minimal marginal cost of serving an extra user, zero distributional cost and a high ROIC without substantial reinvestment. Its supply-side economies of scale also help it to get network infrastructure and data servers at an extremely cheap rate. That’s why Facebook’s advertisement revenue growth can outpace its expenses by miles.

In short, financials is the aspect that should be least worried in an investment evaluation of Facebook. We expect its financial stability to continue over the next few years and its healthy cash position can help it weather all storms and crises in the future.

Critical points, future prospects and valuation

Critical Points

With all the praises to Facebook, there are certainly some areas that should be always monitored and evaluated. These are the critical points that can undermine Facebook’s business model and future growth.

- Macroeconomic factors and economic recessions

- Facebook’s ability to retain users and user engagement in the future

- Competitors with substantial web traffic that can become another large force

- Facebook as a ‘first-choice’ option to advertisers

- Regulations and data privacy rules

- Users’ sentiment and willingness to hand over their data

- The effectiveness of in-app ad blockers and number of users who use it

- Facebook’s ability to acquire potential threats and copy their features if they can’t acquire it

- Failure to fully monetise WhatsApp and Oculus VR

- Departure of key executives

- Disruptive technology that can transform how people interact and disruptive technology that dramatically improves ad performance

- Facebook’s ability to constantly come up with new ad products

All these aspects should be gauged and monitored from time to time. Any first signs of such events happening deserves a re-evaluation of the company’s fundamental and the ability of management to cope with such events.

Future Prospects

Investing is all about the future, not the past. There begs the question: What is the future of Facebook? Let us look at the projects currently known that may be a revenue driver in the future 5 years:

- Instagram ads

- Facebook Marketplace

- WhatsApp Business and Messenger Business

- Oculus VR

- Roll-out of features that increases product pipeline

- Ads optimisation

- Facebook Watch & Show

- Facebook Group

- Facebook Dating

According to observations of current conditions and my inferences, the areas that will contribute to material revenue growth are Instagram Ads, Roll-out of features that increases product pipeline, Ads optimisation, Facebook Watch & Show, and Facebook Dating

Facebook Marketplace is a nice feature to add to the Facebook Platform. However, it will not be one of the quintessential feature that people surf Facebook for. Because commerce is conducted in the form of discovery, not inquiry (i.e: Amazon), Marketplace will only be the extra feature that Facebook provided. Facebook won’t be marketplace-oriented. Besides, the profit margin made from Marketplace transactions is going to be typically low. These two factors decided that Marketplace will not be the significant revenue driver of Facebook. WhatsApp Business and Messenger Business will likely enjoy strong growth and be embraced by more and more businesses to communicate directly with their customers. But as mentioned before early in this piece, monetisation opportunity remains rather limited. That’s why this research piece thinks that Facebook probably can’t come up with a great monetisation plan for these two apps in the next five years, and therefore, should not be taken into serious consideration in terms of revenue growth. Facebook management had already explained before that Oculus VR will be a project for its 10-year roadmap, so it’s unlikely that Oculus VR will manage to reach mass adoption by consumers and reap great profits in the next five years. Nevertheless, Oculus remains a great opportunity for Facebook and it should be monitored during the next five years to determine how is it progressing. If it progresses well in the next few years and signals a great probability of mass adoption by the public, it will undoubtedly be the golden goose for Facebook in the subsequent five years, beginning the second growth phase of the Facebook empire. Facebook Group is one of the main feature that attract users to spend more time on Facebook (as mentioned before, regional groups and interest groups). Facebook also recently announced that it is experimenting on a revenue-sharing model with group admins to collect a monthly subscription fee for premium groups that have exclusive contents. The other side of the story, meanwhile, is that subscription groups are just minorities among the many groups on Facebook, and one of the reasons that Facebook groups thrive is because they are free! Due to this reason, we concluded that the impact on Facebook Group subscriptions will have negligible impact on its bottom line.

After discussing the why-nots, let’s dive into the main revenue driver for the future five years. While Facebook is already a video-oriented social networking platform most of the time, revenue from videos has not reach its full potential. On top of that, Facebook is spending aggressively on video contents on Facebook to build its own video ecosystem, named Facebook Watch & Show. Facebook Watch & Show is providing content creators a chance to popularise their content on Facebook in the form of shows that contain episodes. As Youtube is already crowded by well-known Youtubers that enjoyed first-mover advantages, it is harder and slower for a completely new content creator to build their fame on Youtube as compared to last time. In this scenario, Facebook presents a tantalising opportunity for first-time content creators to accumulate their popularity and spread their work. Indeed, Facebook’s socialising characteristics and sharing feature also enables videos to go viral like a wildfire through compounded sharing. A few content creators such as Wil Aime and QPark have already build their fan base and popularity through Facebook’s video platform and so, it is expected that Facebook Watch & Show can attract more and more creators and grow significantly in the future years. Besides, video-based ad products are also more interactive and typically have a higher chance to attract users’ attention, therefore the shift of more advertising revenue to video ads is anticipated. Based on the above reasoning, we believe that more video-based ad products and monetisation (i.e: revenue-sharing with creators) will follow if its video ecosystem can grow as anticipated.

Another catalyst for growth is value optimisation of ads, mostly through better retargeting efforts, such as Dynamic Ads on Facebook. Value optimisation of ads can be achieved by having more user information and data; and we believe that Facebook’s management has the ability to come up with innovative ads that present more value for advertisers. High-value ads will definitely attracts adoption of more advertisers and command higher profit margins for the company. We anticipate Facebook’s dynamic ads series to continue to expand and more similar offerings to be rolled out.

In the last few months, Facebook had announced its ambitious plan to go into the online-dating market. This move, although shocking, should not be all that shocking. Facebook has a large pile of data about user interests, user preferences and user behaviour. Matching is the core of all dating apps. Whichever dating app that can create a matching mechanism several times better than its competitor can dominate the online dating market. Hence, if Facebook can successfully utilise the data it possesses to make the matching mechanism more efficient than other competitors in the dating market, it can be yet another market leader. Furthermore, the dating feature will be inside Facebook’s app, so that its already-enormous user base will be one of its competitive advantage. This move is a sensible one, leveraging Facebook’s advantage to gain ground in a nascent and growing market, with low upfront cost and development expenses. In the worst case scenario, Facebook’s matching mechanism will be of the same quality of other dating apps, and even in this case its sheer size will still help it to gain a foothold in the dating market. A low risk-high reward move indeed. Although Facebook has publicly announced that it won’t collect any user data and make money on this feature, great monetisation and strategic opportunities still lies ahead. The most important thing is to generate regional network effects and build a well-functioned dating platform, and profits will follow.

Last but not least, another robust pipeline of growth that can be anticipated and highly probable to materialise is the expanding growth of Instagram ads. Facebook just started mass monetisation effort on Instagram in 2016 and Instagram now commands $3.64B of revenue. As more advertisers embrace Instagram, and Instagram ads generally have a higher profit margin as compared to Facebook ads, it is expected that its contribution to revenue will continue to grow. With this said, revenue growth from Instagram is already anticipated by the markets and we believed that it’s already fully priced. Nonetheless, it is believed that Instagram’s management will have the ability to roll out more features on their products to attract users and increase their product offerings to advertisers. Although the market is excited and holding high hopes on the newly introduced IGTV feature, a video platform, we hold a more sceptical and less optimistic view on it. This is because IGTV is more of a platform for Instagram celebrities and influencers to promote themselves and engage with more Instagram users, we hold the view that it will continue to be this kind of niche platform (resembles more of Snapchat’s Discover feature) rather than an all-encompassing platform such as Youtube, or even Facebook Watch & Show. The monetisation opportunity is definitely there, but less significant and of minimal impact.

After discussing the potential growth areas, we must anticipate the expenditures made in the future five years. Facebook’s management had explicitly stated that huge amounts of investment will be spent on video content and fact-checking programmes in the next few years. Therefore, with the information we have, it is extrapolated that future expenditure sources will be from:

- Investment on video content for Facebook’s video platform

- Investment on content for Oculus VR

- Fact-checking programmes to maintain ecosystem health

- Investment on network infrastructure and data centres to support user growth in APAC and Rest of World (RoW) region

Therefore, we expect significant investments on content will have effects on its bottom line and net profit as a share of total revenue may come down in the next two or three years. However, it is still highly probable that Facebook’s revenue growth will outpace its spending on investments and the upbeat of net profit in absolute amount will still continue strong.

Another aspect to take note here is the noticeable disparity between major user growth coming from APAC region and developing nations and major advertising revenue coming from advertisers in the U.S, Canada and Europe. This is shown in the ARPU of Facebook in its Q1 2018 report.

Hence, the main point here is that total ad revenue growth by U.S and Canada users must exceeds the total expenses of serving APAC and RoW users. In this research entity’s opinion, this is not something to worry about, just something to take note. Also, because excessive ads displayed to user will harm user sentiment, Facebook must roll out innovative ad products and diversify their products pipeline so that user sentiment won’t be harmed.

There are also two industry-wide factors affecting Facebook’s revenue: a broad trend of revenue shift to digital advertising (tailwind) and an economic recession (headwind). An economic recession is highly likely to hit the U.S economy in the future few years and it will definitely hampers Facebook’s profits. However, that is also a great opportunity for investors to cash in Facebook’s stock at a great price

Overall, in the course of the next few years, there will certainly be new products and new features that will be announced. Changes will occur and hurdles will be met. Therefore, what we are betting on is primarily Facebook’s management to overcome hindrances and their ability to continuously come up with great products and features to maintain their user platform dominance and ad revenue growth

Valuation

I would like to apologise here for my inability to come up with a detailed valuation model based on numbers and figures, due to my lack of knowledge in valuation modelling. Therefore, take my fair value of Facebook with a huge grain of salt and find more believable people to reach a better conclusion on its appropriate buying price.

Because of my deficiencies, I decided to determine whether the current price ($200 per share) is a fair price for Facebook based on market participants’ anticipation and assumptions about Facebook Inc. After scanning through many analyst reports and market opinions, my conclusion is that Facebook is slightly overvalued and that market participants have held very high expectations on its financial performances, leaving little margin of error for things to go wrong. Although it is likely that Facebook will be able to hit their expectations if everything goes right and if the economic condition is in good shape, we don’t feel comfortable with its thin margin of safety (in terms of market expectations).

Furthermore, we believe that over the next 2 – 3 years, there will be better buying opportunities and the probability of a recession coming largely increases. Therefore, we believe that now is not the best time to buy Facebook stocks, and thinks that our patience will promise us great opportunities. In conclusion, we believe that the price range of $170 and below will an acceptable price.

And that’s the end of my research. Thank you for taking such a long time to read my analysis on Facebook Inc. I would like to apologise again for the many incompetences and deficiencies in this piece of analysis, I strive to address these shortcomings in my future investment analysis. Also, I will publish my reflections and post-mortem review shortly after this as i think that my mistakes and weaknesses can provide useful insights and thoughts to others seeking to perfect their investment analysis process. If you have any thoughts and opinions about this research piece, you can email yiyangchuah321@gmail.com to discuss your ideas with me. Once again, thank you for your precious time and patience 🙂

Central Assumptions:

Critical mass numbers unknown – thus estimated to be 10% of users (conservative)

Although Instagram is already fairly penetrated in the U.S, Canada and western countries, we can still expect to see it enjoying decent growth in Asia Pacific region and other countries in the world

The law of Divine Discontent exists in the social network industry

Oculus VR will remain immaterial to Facebook’s bottom line and stock performance in the next 5 years, given its importance in Facebook’s long-term roadmap

WhatsApp and Messenger presents limited monetisation opportunities over the next five years

Obtaining user consent to access data won’t be an issue in the future due to user ignorance in the near term and user laziness in the longer term